1Understanding What Your Home Insurance Policy Actually Covers

You pay for home insurance every month — but do you actually know what your policy covers? Most Canadian homeowners have a general sense that their insurance protects their house, but the specifics are often unclear until they need to file a claim.

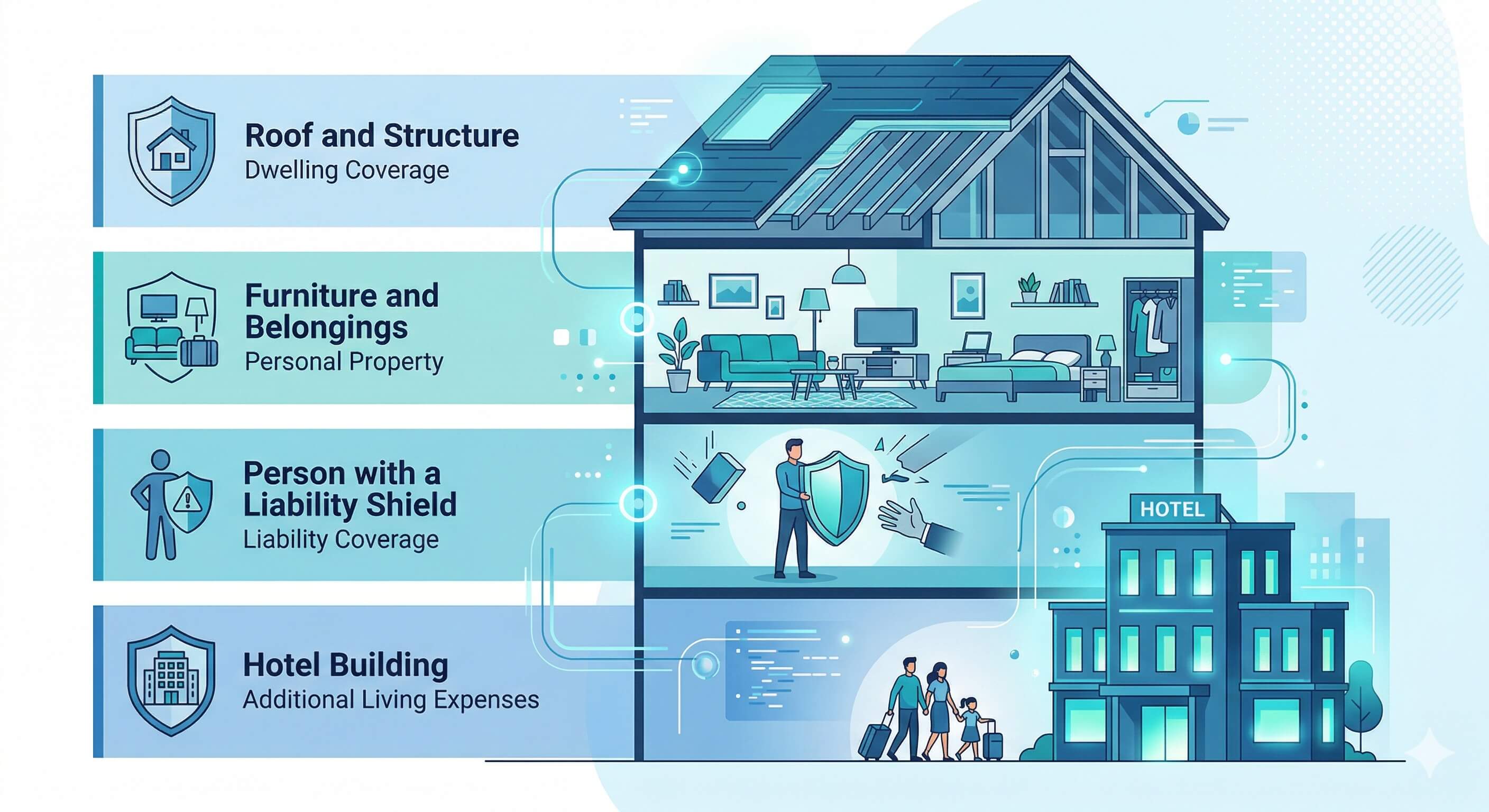

A standard home insurance policy in Canada is more comprehensive than many people realize. It doesn't just cover the physical structure of your home — it also protects your personal belongings, shields you from liability if someone is injured on your property, and pays for temporary living expenses if your home becomes uninhabitable.

But it also has important limitations. Understanding what's included — and what's not — is the difference between being properly protected and facing a devastating financial surprise when something goes wrong.

In this guide, we'll break down every component of a standard Canadian home insurance policy, explain the different types of coverage available, and help you understand how to make sure you have the right protection for your home and family.

2Dwelling Coverage: Protecting the Structure of Your Home

Dwelling coverage is the foundation of every home insurance policy. It pays to repair or rebuild the physical structure of your home if it's damaged or destroyed by a covered peril.

What dwelling coverage includes

Dwelling coverage protects:

- The main structure of your home — walls, roof, floors, foundation

- Attached structures — an attached garage, deck, or porch

- Built-in appliances and fixtures — furnaces, water heaters, built-in cabinetry, plumbing, and electrical systems

- Permanent installations — flooring, countertops, and built-in shelving

Common perils covered under dwelling coverage

Depending on your policy type, dwelling coverage typically protects against:

- Fire and smoke damage

- Windstorm and hail

- Lightning strikes

- Theft and vandalism

- Falling objects (e.g., a tree landing on your roof)

- Weight of snow and ice

- Sudden and accidental water damage (burst pipes, appliance overflow)

- Explosion

How dwelling coverage is calculated

Your dwelling coverage limit should be based on the replacement cost of your home — the amount it would cost to rebuild your home from the ground up at today's construction prices. This is different from your home's market value or the price you paid for it. Replacement cost accounts for current material costs, labour, and any building code upgrades required during reconstruction.

It's critical to review your dwelling coverage limit regularly, especially as construction costs rise. Many insurers offer an inflation guard endorsement that automatically adjusts your coverage limit each year.

3Personal Property Coverage: Protecting Your Belongings

Personal property coverage protects the contents of your home — everything from furniture and clothing to electronics, appliances, and personal items. If your belongings are damaged, destroyed, or stolen due to a covered peril, this coverage pays for their repair or replacement.

What personal property coverage includes

- Furniture and home decor

- Clothing and shoes

- Electronics — TVs, computers, tablets, smartphones

- Kitchen appliances and cookware

- Books, sporting goods, and hobby equipment

- Linens, bedding, and towels

- Tools and lawn equipment

Replacement cost vs. actual cash value

There are two ways insurers calculate personal property payouts:

- Replacement cost: Pays to replace your item with a new one of similar kind and quality, without deducting for depreciation. This is the better option.

- Actual cash value (ACV): Pays the current value of the item, factoring in depreciation. A five-year-old laptop might only be worth a fraction of what you paid for it.

Always opt for replacement cost coverage if your insurer offers it. The premium difference is modest, but the payout difference can be enormous.

Sub-limits to watch for

Standard policies place sub-limits — maximum payouts — on certain categories of high-value items:

- Jewelry: Typically capped at $1,000–$6,000 total

- Bicycles: Often limited to $1,000–$2,000

- Cash and securities: Usually capped at $200–$500

- Collectibles and art: May have low sub-limits unless specifically scheduled

- Business equipment: Often limited or excluded entirely

If you own high-value items that exceed these sub-limits, you'll need a scheduled items endorsement (also called a floater or rider) to ensure full coverage.

4Liability Coverage: Protection Against Lawsuits and Legal Claims

Liability coverage is one of the most important — and most overlooked — components of a home insurance policy. It protects you financially if someone is injured on your property or if you or a member of your household accidentally cause damage to someone else's property.

What liability coverage protects against

- A visitor slips on your icy walkway and breaks a hip

- Your child accidentally breaks a neighbour's window while playing

- Your dog bites a guest or a passerby

- A tree from your property falls onto a neighbour's fence or car

- Someone is injured using your swimming pool or trampoline

What's included in a liability claim payout

Liability coverage Canada homeowners rely on typically pays for:

- Legal defence costs — lawyer fees, court costs, and related expenses

- Settlements and judgments — amounts you're ordered to pay to the injured party

- Medical payments — immediate medical expenses for a person injured on your property, regardless of who is at fault (often called "no-fault medical payments")

How much liability coverage do you need?

Standard home insurance policies in Canada typically include $1 million in liability coverage. However, many insurers and financial advisors recommend increasing this to $2 million, especially if you:

- Own a home with a pool, trampoline, or other attractive nuisances

- Have a dog (certain breeds may increase risk)

- Frequently entertain guests

- Have significant personal assets to protect

For even higher coverage, you can add an umbrella policy that provides an additional layer of liability protection beyond your home insurance limit. According to the Insurance Bureau of Canada (IBC), most Canadians should carry at least $1 million in liability coverage, and many would benefit from more.

5Additional Living Expenses: Coverage When You Can't Live at Home

If a covered peril — such as a fire, severe windstorm, or major water damage — makes your home uninhabitable, additional living expenses (ALE) coverage pays for your temporary living costs while your home is being repaired or rebuilt.

What ALE covers

- Temporary accommodation — hotel stays or short-term rental costs

- Increased food costs — restaurant meals or grocery expenses above your normal food budget (since you may not have a kitchen)

- Storage costs — fees for storing your belongings while your home is uninhabitable

- Additional transportation — if your temporary location is farther from work or school

- Pet boarding — if your temporary accommodation doesn't allow pets

ALE limits

Most policies cap ALE at a percentage of your dwelling coverage — commonly 20% to 30%. So if your dwelling is insured for $500,000, your ALE limit might be $100,000 to $150,000. There may also be a time limit, such as 12 or 24 months.

Important: ALE only covers the difference between your normal living expenses and your increased costs. If your mortgage payment stays the same, that's not covered by ALE — but a hotel room that costs more than your normal housing expenses would be.

6Named Perils vs. Comprehensive vs. All-Risk: Understanding Policy Types

Not all home insurance policies offer the same level of protection. The key difference lies in how they define what's covered. In Canada, there are three main policy types:

1. Named Perils (Basic)

A named perils policy only covers risks that are specifically listed in the policy. If a peril isn't named, it isn't covered. Common named perils include:

- Fire and lightning

- Windstorm and hail

- Explosion

- Theft

- Vandalism

- Smoke damage

- Impact by vehicles or aircraft

Named perils policies are the most affordable option, but they provide the narrowest coverage. If something damages your home and it's not on the list, you're on your own.

2. Comprehensive (Broad)

A comprehensive policy — sometimes called a "broad" policy — is a hybrid. It provides all-risk coverage for the dwelling (your home's structure) and named perils coverage for your personal property (your belongings).

This means your house is protected against virtually anything except explicitly excluded perils, while your belongings are only covered for the specific risks listed in the policy. Comprehensive is the most popular choice among Canadian homeowners.

3. All-Risk (Special)

An all-risk policy provides the broadest protection. Both your dwelling and your personal property are covered against all perils except those specifically excluded in the policy. Common exclusions still apply — earthquake, overland flooding, wear and tear, intentional damage — but everything else is covered.

All-risk policies cost more, but they leave far fewer gaps in your protection. If you want maximum peace of mind, this is the policy type to choose.

| Policy Type | Dwelling Coverage | Personal Property Coverage | Cost |

|---|---|---|---|

| Named Perils | Named perils only | Named perils only | Lowest |

| Comprehensive | All-risk | Named perils | Mid-range |

| All-Risk | All-risk | All-risk | Highest |

7What Standard Home Insurance Does NOT Cover

Even the most comprehensive home insurance policy has exclusions. Understanding these gaps is just as important as knowing what's covered. Here are the most common exclusions:

- Overland flooding: Damage from rivers, lakes, or surface water runoff is not included in standard policies. A separate flood endorsement is required.

- Earthquake damage: Not covered in any standard policy. Available as an add-on, especially important in British Columbia and parts of Quebec.

- Sewer backup: Water damage from backed-up sewers or drains requires a separate endorsement.

- Gradual damage: Slow leaks, mould from long-term moisture, and general wear and tear are maintenance issues — not insurable events.

- Pest and vermin damage: Damage from rodents, insects, raccoons, or other pests is excluded.

- Intentional damage: Any damage you cause deliberately is never covered.

- Home-based business equipment: Standard policies may not cover business-related property. You may need a separate rider or commercial policy.

- Vacant home exclusions: If your home is unoccupied for an extended period (typically 30+ days), certain coverages may be voided.

We've written a detailed guide on this topic: 10 Things Your Home Insurance Doesn't Cover. If you're a homeowner, it's essential reading.

8Optional Endorsements You Should Consider

Standard home insurance coverage handles the most common risks, but optional endorsements (also called riders or add-ons) let you tailor your policy to fill specific gaps. Here are the most valuable endorsements to discuss with your insurer:

Water and flood protection

- Overland water/flood endorsement: Covers damage from surface water flooding — increasingly important as extreme weather events become more common across Canada.

- Sewer backup endorsement: Covers damage caused by sewer or drain backup into your home. One of the most commonly claimed endorsements.

Earthquake coverage

Essential if you live in a seismically active area like British Columbia or parts of Quebec and Ontario. Earthquake endorsements typically carry a higher deductible (often 5%–15% of dwelling coverage).

Scheduled items / valuable articles

If you own jewelry, fine art, collectibles, musical instruments, or other high-value items that exceed your policy's sub-limits, a scheduled items endorsement provides full coverage up to an agreed-upon value — often with no deductible.

Home-based business endorsement

If you work from home or run a business out of your property, a standard policy may not cover your business equipment or liability. A home-based business endorsement extends protection to your work-related property and activities.

Identity theft coverage

Some insurers offer endorsements that cover expenses related to identity theft — legal fees, lost wages, and the cost of restoring your credit.

Service line coverage

Covers the cost of repairing or replacing utility lines (water, sewer, electrical) that run between your home and the municipal connection. These are your responsibility as a homeowner, and repairs can cost thousands of dollars.

Endorsements typically add only a few dollars per month to your premium but can save you tens of thousands in the event of a claim. Review your policy annually and discuss any coverage gaps with your broker.

9How to Determine the Right Coverage Amount

One of the most critical decisions you'll make when purchasing home insurance is choosing the right coverage amounts. Underinsuring your home can leave you with a devastating shortfall, while overinsuring means paying for protection you don't need.

Dwelling coverage: Replacement cost, not market value

Your dwelling coverage should reflect the full replacement cost of your home. This is the cost to rebuild your home from scratch — including materials, labour, debris removal, and any building code upgrades — at current prices.

Do not confuse replacement cost with:

- Market value: Includes land value, location desirability, and market conditions — none of which affect rebuild cost

- Purchase price: What you paid for the home, which may be higher or lower than the current rebuild cost

- Mortgage amount: Your outstanding loan balance has nothing to do with how much it costs to rebuild

Ask your insurer to perform a replacement cost estimate, or hire an independent appraiser. Review this figure every 2–3 years, as construction costs change.

Personal property: Do a home inventory

Walk through every room in your home and estimate the replacement cost of everything you own. Most people significantly underestimate this figure. A thorough home inventory should include:

- Room-by-room list of all items

- Photos or video of your belongings

- Receipts for high-value items

- Serial numbers for electronics

Store your inventory in the cloud or off-site, so it's accessible even if your home is destroyed.

Liability: Go higher than the minimum

Standard policies include $1 million in liability coverage, but if you have significant assets, a pool, a dog, or regularly host guests, consider increasing to $2 million or adding an umbrella policy. The cost to increase from $1M to $2M is typically only a few dollars per month.

For tenants, the same principle applies — though the focus shifts to personal property and liability rather than dwelling coverage.

10Final Thoughts: Know What You're Paying For

A home insurance policy is one of the most important financial safety nets you can have. It protects your home, your belongings, and your financial future — but only if you understand what's included and make sure your coverage matches your actual needs.

Here's a quick summary of what standard home insurance coverage includes:

- Dwelling coverage — rebuilds or repairs the physical structure of your home

- Personal property coverage — replaces your belongings if damaged, destroyed, or stolen

- Liability coverage — protects you from lawsuits and legal claims

- Additional living expenses — pays for temporary housing when your home is uninhabitable

Take the time to review your policy, understand your endorsements, and verify that your coverage limits are accurate. If you haven't looked at your policy in more than a year, now is the time.

Insurance isn't something you want to learn about the hard way. Know your coverage before you need it — and make sure there are no surprises when it matters most.

Powered by Bluecouch

Build the Exact Coverage Your Home Needs — No Guesswork

- Bluecouch walks you through every coverage type before you commit

- Easily add overland flood, sewer backup, and liability endorsements

- See what each provider covers and compare side by side

- Get a complete home insurance quote tailored to your property in 90 seconds

Frequently Asked Questions

A standard home insurance policy in Canada includes four main types of coverage: dwelling coverage (the physical structure of your home), personal property coverage (your belongings), personal liability coverage (protection if someone is injured on your property or you cause damage to others), and additional living expenses coverage (temporary housing costs if your home becomes uninhabitable due to a covered peril).

It depends on the source. Standard home insurance typically covers sudden and accidental water damage — such as a burst pipe or an overflowing appliance. However, overland flooding from rivers, lakes, or heavy rainfall is usually excluded from basic policies. You can add a water/flood endorsement to your policy for additional protection. Sewer backup coverage is also available as an optional add-on.

Your dwelling coverage should equal the full replacement cost of your home — the amount it would cost to rebuild from the ground up at current construction prices, not the market value or purchase price. This figure accounts for materials, labour, and building code upgrades. Your insurer or a professional appraiser can help you determine the correct replacement cost.

Named perils coverage only protects against risks specifically listed in your policy, such as fire, theft, windstorm, and hail. All-risk (also called comprehensive) coverage protects against all perils except those explicitly excluded, such as earthquakes and floods. All-risk policies offer broader protection and are generally recommended for homeowners who want fewer coverage gaps.

Yes. Most home insurance policies include off-premises coverage for your personal belongings, meaning your items are protected even when they're away from home — for example, if your luggage is stolen during a trip or a laptop is taken from your car. However, off-premises coverage is usually limited to a percentage of your total personal property coverage (commonly 10%), and certain sub-limits still apply.

Find out exactly what coverage you need. Get a personalized home insurance quote in minutes.

Get Your Quote