1Why Your Insurance Payout Might Be Less Than You Expected

You file a home insurance claim expecting to be made whole. Then the cheque arrives — and it's far less than what it'll actually cost to fix or replace what you lost.

Welcome to insurance depreciation: one of the most misunderstood parts of a home insurance policy, and one of the most costly surprises at claim time.

In this guide, we'll explain exactly what depreciation means in a home insurance context, the critical difference between recoverable and non-recoverable depreciation, how insurers calculate it, and — most importantly — how to make sure you're not left covering the gap out of your own pocket.

2What Is Depreciation in Home Insurance?

In insurance, depreciation is the reduction in the value of your property or belongings over time due to age, wear and tear, and obsolescence.

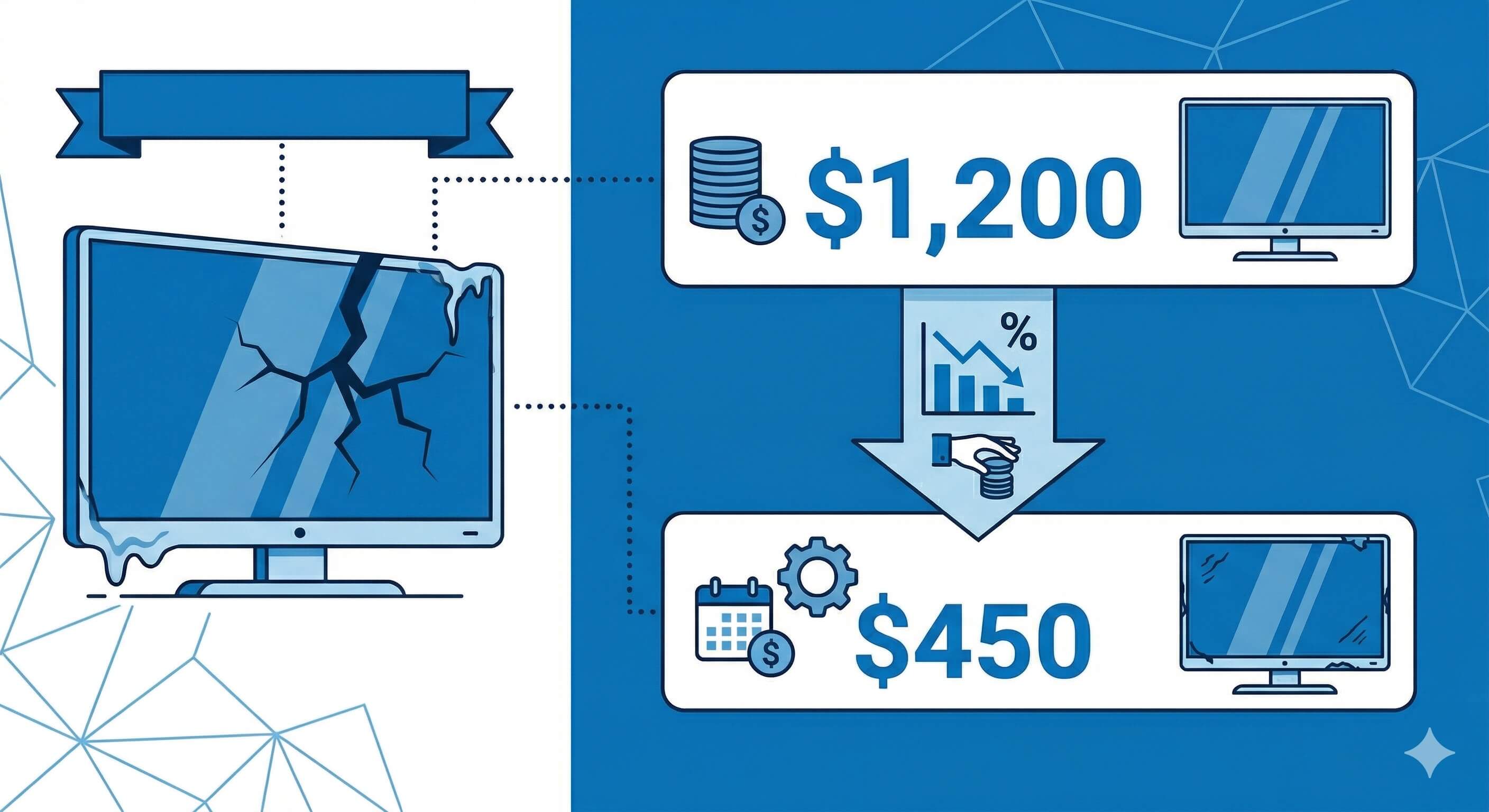

Think of it this way: a dishwasher you bought for $1,200 eight years ago isn't worth $1,200 anymore. It's older, used, and could fail any day. An insurer using depreciation would calculate what that dishwasher is worth today — perhaps $400 — and that's what they'd pay if it was destroyed in a covered event.

Depreciation affects:

- Personal belongings — electronics, appliances, furniture, clothing

- Structural components — roof, HVAC, plumbing, electrical systems

- The dwelling itself (under some policy types)

How much depreciation is applied — and whether any of it is recoverable — depends on the type of insurance coverage you have.

3Actual Cash Value (ACV) vs. Replacement Cost Value (RCV)

The single most important factor determining your depreciation exposure is whether your policy pays Actual Cash Value (ACV) or Replacement Cost Value (RCV).

Actual Cash Value (ACV)

ACV policies pay you what the damaged item was worth at the time of loss — accounting for age and depreciation. The formula is simple:

ACV = Replacement Cost − Depreciation

Example: Your 7-year-old laptop (originally $1,500, expected lifespan 5 years) is stolen. The insurer calculates it's fully depreciated and pays you close to $0. You're left buying a new laptop entirely out of pocket.

ACV policies have lower premiums, but they leave you exposed to large out-of-pocket costs for older items.

Replacement Cost Value (RCV)

RCV policies pay you what it actually costs to replace the damaged item with a new equivalent today. There's no permanent deduction for age.

Example: That same 7-year-old laptop. Under an RCV policy, the insurer pays you what a comparable new laptop costs today — say $1,400 — not its depreciated value.

RCV policies cost more in premiums, but they eliminate the depreciation gap at claim time.

| ACV Policy | RCV Policy | |

|---|---|---|

| Premium cost | Lower | Higher ($100–$300/yr more) |

| Claim payout | Depreciated value | Full replacement cost |

| Out-of-pocket gap | Large (especially older items) | Minimal |

| Best for | New homes, new belongings | Most homeowners |

4What Is Recoverable Depreciation?

Recoverable depreciation is the portion of depreciation that your insurer withholds from your initial claim payment — but will pay you back once you prove you've completed the repairs or replacement.

Here's how it works in practice:

- You suffer a covered loss — say, a hail storm damages your roof.

- Your insurer estimates the full replacement cost at $18,000.

- Your roof is 12 years old with a 25-year lifespan — it's 48% depreciated.

- The insurer sends an initial cheque for the ACV: $18,000 − $8,640 depreciation = $9,360.

- You hire a contractor and replace the roof. Total cost: $18,000.

- You submit the invoices to your insurer within the required timeframe (typically 6–12 months).

- Your insurer releases the withheld depreciation: $8,640.

- Your total payout: $18,000 (minus your deductible).

Recoverable depreciation is only available on Replacement Cost Value (RCV) policies. If you have an ACV policy, all depreciation is non-recoverable.

Key rule: You must actually complete the repair or replacement to claim recoverable depreciation. If you pocket the initial ACV payment and don't rebuild, the withheld amount is forfeited.

5What Is Non-Recoverable Depreciation?

Non-recoverable depreciation is the portion of value loss that your insurer will never pay out — regardless of whether you replace the item.

It applies in two situations:

- ACV policies: All depreciation is non-recoverable. You receive the depreciated value and nothing more.

- RCV policies with exclusions: Some items may be subject to non-recoverable depreciation (e.g., items past their useful lifespan, or specific categories like roofing materials in certain provinces).

Non-recoverable depreciation is most painful for:

- Roofs — older roofs can be 60–80% depreciated, meaning you receive only 20–40% of replacement cost

- HVAC systems — furnaces and air conditioners depreciate significantly after 10+ years

- Electronics — high depreciation rates (20–30%/year) make older devices nearly worthless under ACV

6How Do Insurance Companies Calculate Depreciation?

Insurers use a combination of the item's age, its expected useful lifespan, and internal depreciation schedules to arrive at a depreciated value.

The basic formula:

Annual Depreciation Rate = 100% ÷ Expected Lifespan (years)

Total Depreciation = Annual Rate × Age of Item

Common Depreciation Schedules

| Item | Expected Lifespan | Annual Depreciation |

|---|---|---|

| Asphalt shingle roof | 20–25 years | 4–5%/year |

| Furnace / HVAC | 15–20 years | 5–7%/year |

| Refrigerator / Appliances | 10–15 years | 7–10%/year |

| Laptop / Computer | 3–5 years | 20–33%/year |

| TV / Electronics | 5–7 years | 14–20%/year |

| Clothing | 2–5 years | 20–50%/year |

| Furniture | 10–15 years | 7–10%/year |

These figures vary by insurer. Some companies cap depreciation at a maximum percentage (e.g., never more than 80% depreciated), while others apply depreciation more aggressively.

If you believe your insurer's depreciation calculation is too aggressive, you have the right to dispute it — and providing receipts, photos, or an independent appraisal can strengthen your position.

7How to Recover Depreciation on a Home Insurance Claim

If you have an RCV policy and have received your initial ACV payout, follow these steps to claim your recoverable depreciation:

- Review your claim settlement letter. It should show the full replacement cost estimate, the depreciation withheld, and your initial ACV payment. Keep this document.

- Complete the repair or replacement. You must actually replace or fix the damaged item — you cannot simply pocket the ACV and claim the withheld depreciation later.

- Keep all receipts and invoices. You'll need documented proof of what you spent to submit to your insurer.

- Submit a Proof of Replacement. Contact your insurer or claims adjuster and submit your invoices, contractor receipts, or purchase receipts within the required timeframe (typically 180 days to 1 year from the initial payment date).

- Receive your supplemental payment. Your insurer will review the documents and release the withheld depreciation, up to the original estimate.

Important: If your replacement cost exceeds the original estimate, document everything and request a supplement from your adjuster. Estimates are often conservative and can be negotiated.

8What Is Depreciation Protection (or Depreciation Waiver)?

Some Canadian insurers offer an add-on called depreciation protection, a depreciation waiver, or guaranteed replacement cost. This endorsement removes depreciation from the claim equation entirely — even without requiring you to submit replacement receipts.

Under a depreciation protection endorsement:

- Your initial claim payment is the full replacement cost (not the ACV)

- No withheld depreciation to chase down later

- No receipts required — the full amount is paid upfront

This is the most comprehensive coverage available and is particularly valuable for:

- Homeowners with older roofs, appliances, or HVAC systems

- Anyone who wants claim simplicity and certainty

- Homes with significant personal property value

Cost: Depreciation protection endorsements typically add $100–$250 per year to your premium — a small price relative to the potential payout difference.

95 Tips to Protect Yourself from the Depreciation Gap

- Choose Replacement Cost Value (RCV) coverage over Actual Cash Value (ACV) — the premium difference is small; the claim difference is huge.

- Create a home inventory. Photograph and document your belongings with purchase dates and receipts. This speeds up claims and gives you leverage if you dispute depreciation calculations.

- Ask about depreciation protection endorsements. If your insurer offers a depreciation waiver, consider adding it — especially if your home or contents are more than 5 years old.

- Review your policy's depreciation caps. Some policies cap depreciation at 50% or 75% — others do not. Know your policy before a claim, not after.

- Don't delay replacing damaged items. Recoverable depreciation has a claim window — typically 6 to 12 months. Miss that deadline and the withheld amount is forfeited.

10Bottom Line

Insurance depreciation is the gap between what your insurer pays and what it actually costs to replace your damaged property. Understanding the difference between ACV and RCV policies — and between recoverable and non-recoverable depreciation — is essential to avoiding an expensive surprise after a claim.

For most Canadian homeowners, the right move is to ensure your policy includes Replacement Cost Value coverage, keep a detailed home inventory, and follow the steps to claim your recoverable depreciation if you ever need to file a claim.

If you're not sure what type of coverage you currently have, the best time to find out is now — not when you're filing a claim.

Powered by Bluecouch

Get Full Replacement Cost Coverage — Not a Depreciated Payout

- Compare home insurance policies that include Replacement Cost Value (RCV)

- Avoid the depreciation gap — get paid what it actually costs to replace your belongings

- Kylie, our AI agent, finds the right coverage level for your home in 90 seconds

- Fully online — no brokers, no phone calls, no surprises at claim time

Frequently Asked Questions

Depreciation in insurance refers to the reduction in value of your property or belongings over time due to age, wear, and obsolescence. When you make a claim under an Actual Cash Value (ACV) policy, your insurer pays you what the item was worth at the time of loss — not what it costs to replace it new. The difference between the replacement cost and the ACV payout is the depreciation deducted.

Recoverable depreciation is the portion of depreciation that your insurer withholds from your initial claim payment but will release to you once you prove you've actually replaced the damaged item. It only applies to Replacement Cost Value (RCV) policies. You typically have 6 to 12 months after the initial payment to submit your replacement receipts and claim the withheld amount.

Non-recoverable depreciation is the portion of value loss that your insurer will never pay out, even if you replace the item. This occurs with Actual Cash Value (ACV) policies. For example, if your 8-year-old roof is damaged, the insurer calculates what a roof of that age is worth today — not what a new roof costs — and that gap is permanently non-recoverable.

Insurers typically use the item's age, expected lifespan, and a depreciation schedule to calculate its current value. For example, a roof with a 25-year lifespan that is 10 years old is 40% depreciated. Electronics depreciate faster (often 20–30% per year), while structural components like walls depreciate more slowly. Each insurer has its own depreciation tables.

To receive the full replacement cost, you need a Replacement Cost Value (RCV) policy. After a covered loss, your insurer first pays the ACV (replacement cost minus depreciation). Once you purchase or repair the replacement, submit the receipts within the required timeframe (usually 180 days to 1 year), and the insurer releases the recoverable depreciation — bringing your total payout up to the full replacement cost.

For most homeowners, yes. The cost difference between an ACV and an RCV policy is typically $100–$300 per year, but the financial gap at claim time can be thousands of dollars — especially for roofs, HVAC systems, and appliances. If your home or its contents are more than a few years old, Replacement Cost coverage is strongly recommended.

Get a home insurance quote that includes full Replacement Cost coverage — no surprises at claim time.

Get Your Quote