1The Formula Behind Your Insurance Payout

When your home is damaged and you file an insurance claim, the payout you receive is rarely the sticker price of a brand-new replacement. The difference comes down to one word: depreciation.

Insurance companies use structured formulas and item-specific depreciation schedules to calculate how much your property has declined in value since it was new. Understanding this calculation is essential — not just to know what to expect, but to identify when an insurer's estimate is incorrect and how to challenge it.

In this guide, we break down the exact methodology Canadian insurers use to calculate depreciation, provide detailed depreciation tables for common home items, explain what a "depreciation cheque" from your insurer actually means, and show you how to dispute a calculation you believe is wrong.

2The Core Formula: How Depreciation Is Calculated

Most Canadian insurers calculate depreciation using a straightforward age-to-lifespan formula:

Step 1: Determine the Annual Depreciation Rate

Annual Depreciation Rate = 100% ÷ Expected Useful Lifespan (years)

Example: An asphalt shingle roof with an expected lifespan of 25 years depreciates at 4% per year.

Step 2: Calculate Total Accumulated Depreciation

Total Depreciation % = Annual Rate × Age of Item

Example: A 12-year-old roof at 4%/year = 48% total depreciation.

Step 3: Apply to Replacement Cost

Actual Cash Value (ACV) = Replacement Cost × (1 − Total Depreciation %)

Example: $20,000 replacement cost × (1 − 0.48) = $10,400 ACV

Depreciation Caps and Floors

Most insurers apply limits to their depreciation calculations:

- Maximum depreciation caps: Many insurers will not depreciate an item below a floor value — typically 10–25% of replacement cost. This means even a very old item receives some minimum payout.

- Age caps: Some insurers stop applying additional depreciation once an item has reached its expected lifespan (i.e., a 30-year-old roof on a 25-year schedule is not depreciated further beyond 100% of its expected life).

- Minimum claim payouts: Policy deductibles interact with ACV calculations — if the ACV is less than your deductible, no payment is made.

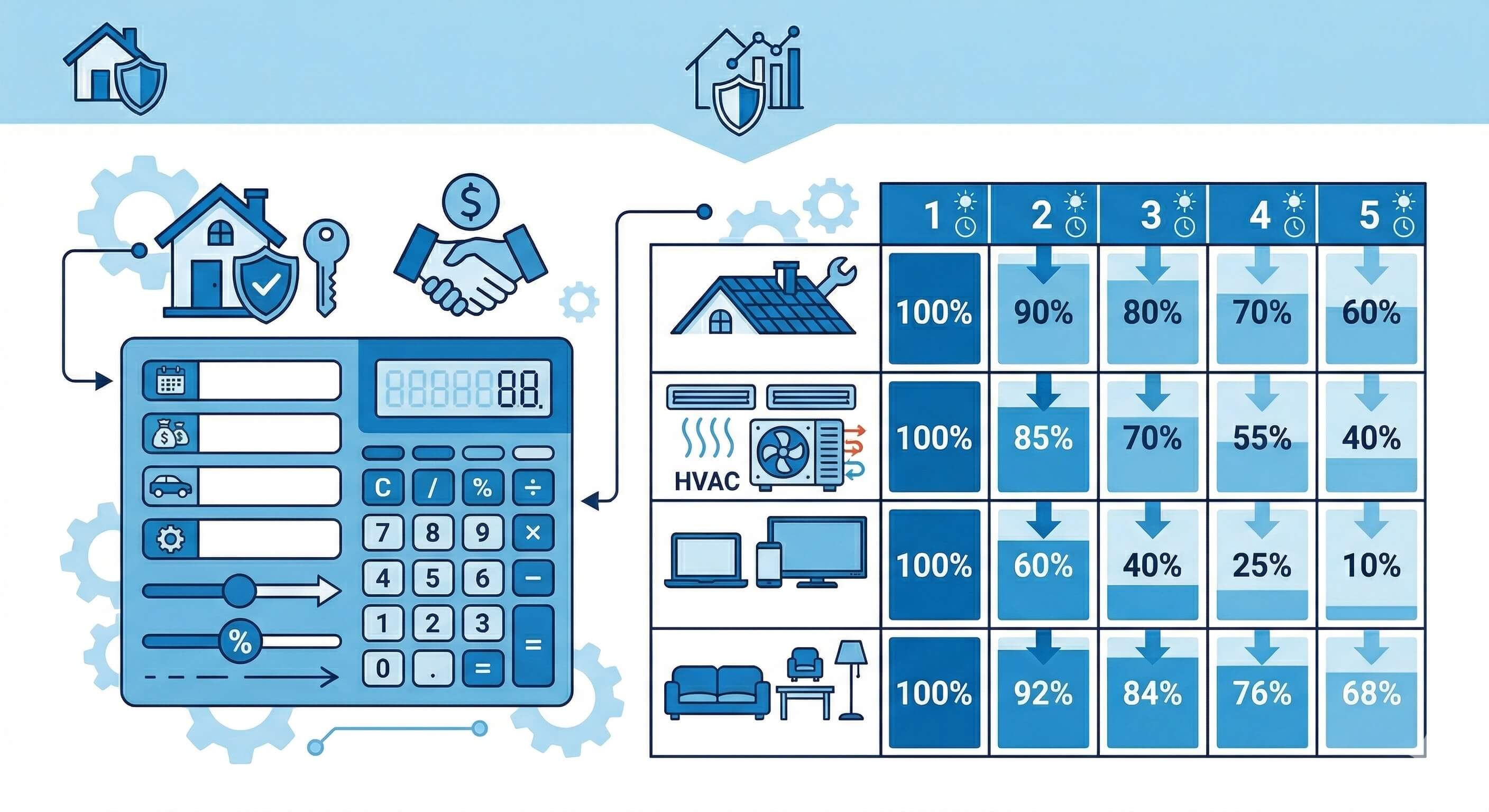

3Depreciation Schedules for Common Home Items

Different items depreciate at very different rates. Here are the schedules most commonly used by Canadian insurers for key categories:

Roofing

| Roof Type | Expected Lifespan | Annual Depreciation Rate |

|---|---|---|

| Asphalt shingles (standard) | 20–25 years | 4–5%/year |

| Asphalt shingles (premium/architectural) | 25–30 years | 3.3–4%/year |

| Metal roofing | 40–50 years | 2–2.5%/year |

| Cedar shakes | 20–25 years | 4–5%/year |

| Flat/EPDM rubber roofing | 15–20 years | 5–6.7%/year |

HVAC and Mechanical Systems

| Item | Expected Lifespan | Annual Depreciation Rate |

|---|---|---|

| Gas furnace | 15–20 years | 5–6.7%/year |

| Central air conditioning | 12–15 years | 6.7–8.3%/year |

| Heat pump | 12–15 years | 6.7–8.3%/year |

| Water heater (tank) | 10–12 years | 8.3–10%/year |

| Water heater (tankless) | 15–20 years | 5–6.7%/year |

| Electric baseboard heaters | 20–25 years | 4–5%/year |

Appliances

| Appliance | Expected Lifespan | Annual Depreciation Rate |

|---|---|---|

| Refrigerator | 10–15 years | 6.7–10%/year |

| Dishwasher | 8–12 years | 8.3–12.5%/year |

| Washing machine / dryer | 10–13 years | 7.7–10%/year |

| Stove / oven (gas or electric) | 13–15 years | 6.7–7.7%/year |

| Microwave | 8–10 years | 10–12.5%/year |

Electronics

| Item | Expected Lifespan | Annual Depreciation Rate |

|---|---|---|

| Laptop / desktop computer | 3–5 years | 20–33%/year |

| Smartphone / tablet | 2–4 years | 25–50%/year |

| Flat-screen television | 5–7 years | 14–20%/year |

| Gaming console | 5–7 years | 14–20%/year |

| Home theatre / audio system | 8–10 years | 10–12.5%/year |

Furniture and Flooring

| Item | Expected Lifespan | Annual Depreciation Rate |

|---|---|---|

| Upholstered sofa / sectional | 8–12 years | 8.3–12.5%/year |

| Dining table and chairs | 10–15 years | 6.7–10%/year |

| Bedroom furniture (wood) | 15–20 years | 5–6.7%/year |

| Hardwood flooring | 25–30 years | 3.3–4%/year |

| Laminate / vinyl flooring | 10–15 years | 6.7–10%/year |

| Carpet | 5–8 years | 12.5–20%/year |

Clothing and Textiles

| Item | Expected Lifespan | Annual Depreciation Rate |

|---|---|---|

| General clothing | 2–5 years | 20–50%/year |

| Outerwear (coats, jackets) | 5–8 years | 12.5–20%/year |

| Footwear | 2–4 years | 25–50%/year |

Note: These figures represent typical ranges used by Canadian insurers. Your specific insurer's depreciation schedule may differ. Request your insurer's schedule in writing if you want to know the exact rates applied to your claim.

4Worked Example: A Multi-Item Claim in Toronto

To see how depreciation calculations play out across a real claim, consider a homeowner in Toronto who suffers a kitchen fire that damages the following items:

| Item | Age | Lifespan | Replacement Cost | Depreciation % | ACV Payout |

|---|---|---|---|---|---|

| Refrigerator | 9 years | 12 years | $2,400 | 75% | $600 |

| Dishwasher | 7 years | 10 years | $1,200 | 70% | $360 |

| Kitchen cabinets | 15 years | 30 years | $14,000 | 50% | $7,000 |

| Laminate flooring | 9 years | 12 years | $4,500 | 75% | $1,125 |

| Microwave | 6 years | 9 years | $350 | 67% | $116 |

| Total | $22,450 | $9,201 |

Under an ACV policy, this homeowner receives $9,201 (minus deductible) for a loss that will cost $22,450 to replace — leaving a gap of over $13,000 out of pocket. Under an RCV policy, the $13,249 depreciation withheld is recoverable upon proof of replacement.

5What Is a Depreciation Cheque From Your Insurer?

You may encounter the term "depreciation cheque" in two different contexts:

Context 1: The Supplemental RCV Payment

Under a Replacement Cost Value (RCV) policy, your insurer releases the withheld depreciation as a second payment once you submit proof of replacement. This second payment is sometimes informally called the "depreciation cheque" — it's the money that was held back from your initial ACV payment and is now being released to you.

This is the good kind of depreciation cheque — it brings your total payout up to the full replacement cost.

Context 2: The Initial ACV Payment

Some policyholders use "depreciation cheque" to mean the initial payment itself — i.e., the cheque that reflects depreciation having been deducted. This usage is less precise but common in informal conversation.

If your insurer or adjuster refers to a "depreciation cheque," clarify which they mean: is it the initial ACV payment, or the supplemental release of withheld recoverable depreciation?

6How to Challenge an Insurance Depreciation Calculation

Depreciation calculations are not infallible. Insurers can make errors in the age they assign to an item, the lifespan schedule they use, or the depreciation percentage they apply. Here's how to push back:

Step 1: Request a Written Breakdown

Ask your claims adjuster to provide a line-by-line depreciation schedule showing the age, expected lifespan, annual depreciation rate, and depreciation percentage applied to each item in your claim. This is your right as a policyholder, and it's the foundation for any dispute.

Step 2: Identify Errors

Review the breakdown and look for:

- Incorrect age: The insurer may assume a generic age if you can't prove purchase date. Your receipts, credit card records, or home inspection reports can establish the true age.

- Wrong lifespan: Manufacturer warranties often specify expected lifespans that differ from what the insurer uses. A 30-year architectural shingle warranty is strong evidence against a 20-year lifespan assumption.

- Aggressive depreciation on well-maintained items: Regular maintenance can extend an item's effective lifespan. Service records for your furnace or HVAC system, for example, can support a longer lifespan argument.

Step 3: Submit Your Evidence

Compile your counter-evidence in writing:

- Purchase receipts or installation invoices showing the item's age

- Manufacturer product specifications showing expected lifespan

- Service and maintenance records

- An independent appraisal (for high-value items)

Submit everything to your claims adjuster in a single organised package via email, and request a written response within a specific timeframe (e.g., 10 business days).

Step 4: Escalate if Necessary

If your adjuster refuses to revise the calculation and you believe it is incorrect:

- Request a formal independent appraisal — most Canadian home insurance policies include a binding appraisal clause allowing either party to initiate this process

- File a complaint with your insurer's internal complaints team

- Contact the General Insurance OmbudService (GIO) — a free independent dispute resolution service available to all Canadian insurance consumers

- Contact your provincial insurance regulator: FSRA (Ontario), AMF (Québec), BCFSA (BC), NSFM (Nova Scotia), etc.

7Actual Age vs. Functional Age: A Key Nuance

Most insurers use a simple chronological age when calculating depreciation — how many years have passed since the item was new. However, some policies and adjusters also consider functional age: how worn or effective the item actually is given its maintenance history and condition.

Functional age works both ways:

- Well-maintained items may be assigned a lower functional age — e.g., a 12-year-old furnace that has been professionally serviced every year and has all parts in good working order may be treated as having the depreciation profile of a 10-year-old unit.

- Poorly maintained items may be assigned a higher functional age — e.g., a roof that was never cleaned and shows heavy algae or moss growth may be assessed as older than its actual age.

Keeping maintenance records is therefore doubly valuable: it both supports your claim that an item was in good condition and provides leverage if you need to dispute the insurer's depreciation assessment.

8Know the Numbers Before You Need to Use Them

Understanding how insurance companies calculate depreciation puts you in a far stronger position — both when buying coverage and when filing a claim.

The key takeaways:

- Depreciation is calculated using the item's age, expected lifespan, and a depreciation rate — resulting in an Actual Cash Value that may be far below the cost of replacement

- Older roofs, HVAC systems, appliances, and electronics carry the largest depreciation exposure

- A "depreciation cheque" from your insurer typically refers to the supplemental RCV payment released upon proof of replacement

- You have the right to challenge any depreciation calculation — and supporting documentation makes a significant difference

- The most effective way to eliminate depreciation risk entirely is to have a Replacement Cost Value policy with a depreciation protection endorsement

Before your next renewal, take 10 minutes to review your policy's depreciation terms. The difference between an ACV and RCV policy — particularly on a 15-year-old roof — can be the difference between a manageable claim and a financially devastating one.

Powered by Bluecouch

Skip the Depreciation Calculation Entirely With the Right Policy

- Compare home insurance policies that pay full Replacement Cost — no depreciation deductions, no surprises

- Our AI agent Kylie explains exactly what your coverage pays at claim time before you commit

- Get quotes from leading Canadian insurers in under 2 minutes

- Fully online — instant quotes, instant coverage, no broker fees

Frequently Asked Questions

Insurance companies calculate depreciation using the item's age, its expected useful lifespan, and a depreciation rate or schedule. The basic formula is: Depreciation = (Age ÷ Expected Lifespan) × Replacement Cost. The result is subtracted from the full replacement cost to arrive at the Actual Cash Value (ACV). Each insurer has its own depreciation tables that vary by item category, and some apply a minimum floor (e.g., items are never depreciated below 10–20% of replacement cost).

A 'depreciation cheque' (or depreciation check) typically refers to the supplemental payment released by your insurer after you submit proof that you've replaced damaged property. Under a Replacement Cost Value (RCV) policy, the insurer initially withholds the depreciation amount; the 'depreciation cheque' is the release of that withheld amount once replacement is verified. Some people also use the term to refer to the initial ACV payment itself — which reflects the depreciated value of the damaged property.

Depreciation on an insurance claim is the reduction applied to your payout to account for the age and wear of the damaged item. Instead of receiving the cost to replace the item new, you receive its current market value — which is lower due to the years of use. For example, a 10-year-old furnace is worth far less than a new one, so the insurer deducts the accumulated depreciation from the replacement cost to calculate your payout.

To challenge a depreciation calculation: (1) Request a written breakdown of the age, lifespan, and depreciation rate applied to each item. (2) Provide counter-evidence — purchase receipts showing a different purchase date, maintenance records, manufacturer warranties, or an independent appraisal. (3) Submit a written dispute to your claims adjuster before accepting final settlement. If unresolved, escalate to your insurer's internal complaint process, your provincial insurance regulator, or the General Insurance OmbudService (GIO).

For a standard asphalt shingle roof in Canada, most insurers use a lifespan of 20–25 years, resulting in an annual depreciation rate of 4–5%. A 12-year-old asphalt shingle roof on a 25-year schedule would be 48% depreciated — meaning you'd receive only 52% of the replacement cost under an ACV policy. Metal roofs and other higher-durability roofing materials typically have longer lifespans (40–50 years), resulting in slower depreciation.

Yes. Insurance depreciation calculations are not final until you accept a settlement. If you can demonstrate that the insurer's age assumption is incorrect, that the item was recently serviced or had components replaced, or that the lifespan used is inconsistent with manufacturer specifications, you can negotiate a revised calculation. Providing documented evidence (receipts, service records, warranties) is key to a successful negotiation.

Get a home insurance quote with full Replacement Cost coverage — no depreciation surprises.

Get Your Quote